Mortgage rates are still a hot topic, and for good reason. After the most recent jobs report came in weaker than expected, the bond market reacted almost instantly. As a result, in early August mortgage rates dropped to their lowest point so far this year at 6.55%.

While that may not seem like a huge shift, many buyers have been waiting for rates to ease. Even a modest drop like this gives hope that we may finally see rates trending downward. But what should we realistically expect?

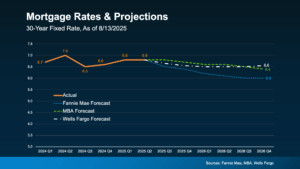

Based on the latest forecasts, rates aren’t expected to decline significantly in the near future. Most experts believe they’ll remain in the mid-to-low 6% range through 2026 (see graph below).

In other words, no major changes are expected. However, small shifts like the one we just saw are still likely. Each time new economic data is released, there’s a chance mortgage rates will adjust. With several key reports coming out this week, we’ll have a clearer picture of where the economy and inflation are headed, as well as how rates may respond.

What Rate Would Get Buyers Moving Again?

The magic number most buyers are watching for is 6%. And it’s not just a psychological benchmark—it has real impact. A recent report from the National Association of Realtors (NAR) found that if rates reach 6%, about 5.5 million more households could afford the median-priced home, and roughly 550,000 people would move forward with buying a home within 12 to 18 months.

That represents a lot of pent-up demand just waiting for the green light. Looking at the graph above, you’ll see Fannie Mae expects we’ll reach that threshold next year. That raises an important question: Does it really make sense to wait for lower rates?

Here’s the tradeoff. If you’re waiting for 6%, chances are many others are too. When rates do move lower and more buyers enter the market all at once, you could face more competition, fewer options, and higher home prices. NAR sums it up this way:

“Home buyers wishing for lower mortgage interest rates may eventually get their wish, but for now, they’ll have to decide whether it’s better to wait or jump into the market.”

Consider the unique window that exists right now. Inventory is up, which means more choices. Price growth has slowed, leading to more realistic pricing. And in many cases, there’s more room to negotiate, giving you the chance to secure a better deal.

These opportunities won’t last if rates fall and demand surges. That’s why NAR explains it this way:

“Buyers who are holding out for lower mortgage rates may be missing a key opening in the market.”

Bottom Line

Rates aren’t expected to reach 6% this year. But when they eventually do, more buyers will return to the market and competition will heat up. If you want less pressure and more negotiating power, that opportunity already exists, and it may not last long. Much of it depends on what happens in the economy next.

Let’s connect to talk about what’s happening in our local market and whether it makes sense to make your move now, before everyone else jumps in.