Saving for a home can feel daunting—especially in today’s market. And for many first-time buyers, the belief that a 20% down payment is required often seems like a major hurdle.

The good news? That’s one of the most common myths about homebuying. Here’s what you really need to know.

Do You Really Have To Put 20% Down When You Buy a Home?

Unless your specific loan program or lender requires it, you likely won’t need to put 20% down to buy a home. In fact, many loan options are specifically designed to help first-time buyers purchase with much less upfront.

For example, FHA loans allow down payments as low as 3.5%, and VA or USDA loans offer qualified applicants—like Veterans—the opportunity to buy with no down payment at all. While putting more down can offer benefits like lower monthly payments or avoiding mortgage insurance, it’s not a requirement. As The Mortgage Reports puts it:

“. . . many homebuyers are able to secure a home with as little as 3% or even no down payment at all . . . the 20 percent down rule is really a myth.”

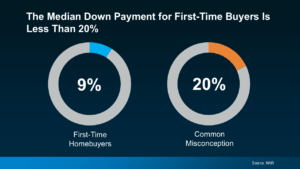

In fact, according to the National Association of Realtors (NAR), the median down payment for first-time homebuyers is just 9%—a far cry from 20%. (See chart below)

The takeaway? You may not need to save as much as you originally thought to buy a home.

Even better—there are numerous down payment assistance programs available that could help bridge the gap. Many first-time buyers don’t realize these options exist, but they can make a big difference in getting you closer to homeownership faster than you expected.

Why You Should Look into Down Payment Assistance Programs

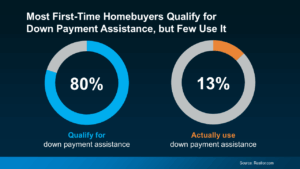

Believe it or not, nearly 80% of first-time homebuyers qualify for down payment assistance (DPA), yet only 13% take advantage of it. That means many buyers are leaving money on the table simply because they don’t know what’s available or how to access it.

That’s a lot of missed opportunity—especially when these programs can offer substantial support. Many provide thousands of dollars that can go directly toward your down payment or closing costs. As Rob Chrane, Founder and CEO of Down Payment Resource, puts it:

“Our data shows the average DPA benefit is roughly $17,000. That can be a nice jump-start for saving for a down payment and other costs of homeownership.”

Just imagine how much further your homebuying budget could stretch with that kind of assistance. In some cases, you might even qualify for more than one program, allowing you to stack benefits and maximize your savings. With that much potential help available, it’s worth exploring all your options.

Bottom Line

Saving up for your first home can feel overwhelming—especially if you’re under the impression that a 20% down payment is a must. The truth? That’s one of the most common homebuying myths. In reality, many loan programs require far less, and there are a variety of down payment assistance options that could give your savings a helpful boost.

To find out what programs you might qualify for and what your options really look like, connect with us! We will help you get you in touch with a trusted local lender who can guide you through the process with clarity and confidence.